If you’ve been lying awake wondering whether your Social Security check is going to disappear, you’re not alone. Millions of Americans are asking the same question right now — and honestly, it’s a fair one.

The headlines are loud. “Social Security Trust Fund Running Out.” “Benefit Cuts Coming.” “2033 Deadline.” It’s enough to make anyone panic and consider claiming benefits the moment they’re eligible, just to get something before the whole thing collapses.

But here’s the thing — panic is rarely a good financial strategy. And the real picture is a lot more nuanced than the headlines suggest.

This guide will walk you through what’s actually happening with Social Security funding, what the numbers really mean for your monthly check, and — most importantly — whether claiming early because of funding worries is actually the right move for you.

What Is the Social Security Funding Cliff — and Why Are People So Worried?

Social Security is funded through payroll taxes. Right now, more money is going out (to current retirees) than is coming in (from workers paying into the system). The program has been drawing down a reserve — called the Trust Fund — to cover that gap.

The problem? That reserve is expected to run dry around 2033. [External Source: SSA.gov Trustees Report]

That’s not a secret. The Social Security Administration has been reporting this for years. But lately, with political gridlock in Washington and the massive Baby Boomer retirement wave in full swing, the anxiety around it has hit a new level.

You’ve probably noticed that conversations about this are everywhere — at family dinners, in financial planning groups, on Reddit threads where near-retirees are genuinely terrified. One person on r/retirement put it bluntly: “I’m 61. Should I just take my benefits now before they cut everything?”

It’s a gut reaction. And it makes emotional sense. But let’s actually look at what depletion means before making any decisions based on fear.

Will Social Security Run Out of Money by 2033?

Short answer: It won’t run out. That framing is misleading.

When the Trust Fund is depleted, Social Security doesn’t shut down. It doesn’t zero out your check. What happens is that the program would only be able to pay out what it collects in payroll taxes each year. [External Source: Congressional Budget Office]

Current projections suggest that it would cover roughly 77–80% of scheduled benefits. So instead of receiving your full projected benefit, you might receive about $0.77–$0.80 for every dollar you were promised.

That’s a significant cut. No one should pretend otherwise. But it’s very different from “Social Security is going away.”

To make this less abstract, here’s the social security insolvency timeline in plain terms:

- 2021: Trust Fund reserves started drawing down faster than projected due to the pandemic’s impact on payroll tax collections

- 2023–2024: SSA Trustees updated depletion estimates to approximately 2033, slightly earlier than prior projections

- 2033 (projected): Trust Fund reserve hits zero; only incoming payroll taxes fund benefits, covering roughly 77–80% of scheduled amounts

- Post-2033: Benefit levels stabilise at that reduced rate — unless Congress acts before or after that point

That last bullet is the one most people miss. It’s not a cliff where everything disappears. It’s a step down that stays at the lower level until legislation changes it.

How Much Will Social Security Benefits Actually Be Reduced in 2033?

Let’s put real numbers on this, because vague warnings aren’t useful.

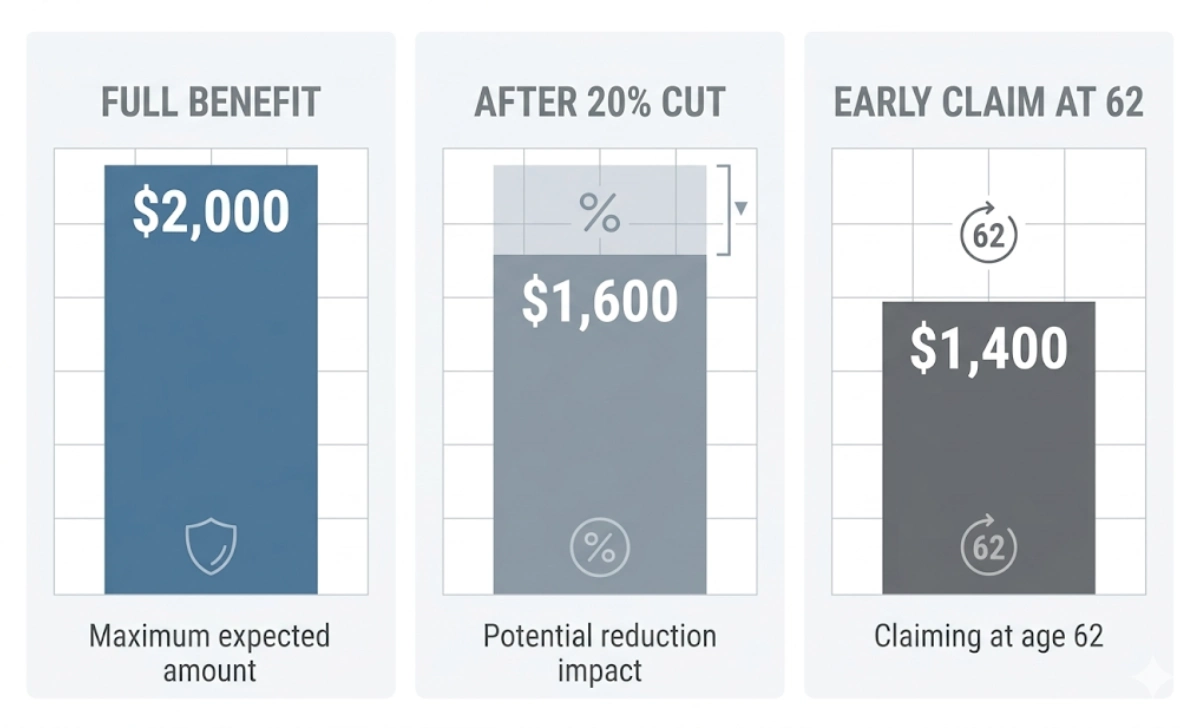

If you’re currently projected to receive $2,000/month at full retirement age, a 20–23% cut would bring that to roughly $1,540–$1,600/month. That’s about $400–$460 less every single month.

For someone living on a fixed income, that gap is real and painful. For someone with a pension, substantial savings, or a working spouse, it might be manageable with adjustments.

Who Gets Hit Hardest?

The impact isn’t equal across the board.

Low-income retirees who depend on Social Security for 80–90% of their income would feel this most severely. There’s simply less financial cushion to absorb a cut.

Higher earners with diverse retirement income sources — a 401(k), IRA, rental income, a spouse still working — are in a much better position to weather a partial reduction.

This distinction matters when you’re deciding whether to claim early. Your personal financial picture is the starting point, not the headlines.

How Will the Social Security Funding Cliff Affect Retirees?

The answer looks pretty different depending on where you are in your retirement timeline — and that context matters more than most guides acknowledge.

If you’re already collecting benefits, you’re somewhat insulated from the decision question. The cut, if it happens, would apply to your existing check — but you’re not facing the “when to claim” dilemma anymore. Your focus should shift to building a cushion that could absorb a potential reduction.

If you’re 55–64 and haven’t claimed yet: You’re in the most complex position. You’re close enough to retirement that this feels urgent, but far enough away that a lot can change between now and 2033. This is the group that most needs a clear-headed decision process rather than a reactive one.

Baby Boomers Already Collecting: Should You Be Worried?

The spike in social security anxiety among baby boomers is real — and it’s showing up in financial planning conversations, retirement forums, and even doctor’s offices as stress-related health concerns. That worry isn’t irrational, but it’s worth separating the emotional response from what the data actually shows.

If you’re already receiving benefits, understand that any changes from Congressional action or automatic cuts would likely come with some protection for current beneficiaries. History supports this — the 1983 reforms, which we’ll get to in a moment, protected people already in the system while adjusting rules for younger workers.

That said, no one can guarantee you. Maintaining some financial flexibility — even a modest emergency fund — is smart regardless.

Near-Retirees (Ages 55–64): Should You Adjust Your Plan?

If you’re in this window, the best move right now isn’t to panic-claim. It’s to stress-test your retirement plan against a scenario where Social Security pays out 20% less than projected. If that scenario breaks your plan entirely, that’s the real problem — and it’s one worth solving now, while you still have time to build other income sources.

Some near-retirees are also turning to remote and contract work as a way to extend their earning years without committing to full-time employment. If you’re considering a career pivot into tech or project management, understanding what hiring managers actually look for is a practical first step — this breakdown of IT project manager interview questions covers the competencies and scenarios employers test for, which is useful whether you’re exploring new roles or simply refreshing your professional footing before retirement.

Can Congress Fix Social Security Before It Runs Out?

The honest answer is: probably yes, but when and how are the unknowns.

Social Security has faced a funding crisis before. In 1983, the system was months from being unable to pay full benefits. Congress passed the Greenspan Commission reforms, which included a gradual increase in the retirement age, taxation of benefits for higher earners, and a payroll tax increase.

It wasn’t pretty. It required both parties to compromise. But it worked, and it pushed the solvency timeline out by decades. [External Source: Social Security Administration Historical Archives]

Current Proposals on the Table

Several legislative ideas are circulating right now:

- Raising or eliminating the payroll tax cap (currently, income above ~$168,600 isn’t taxed for Social Security)

- Gradually increasing the retirement age to 68 or 70 for younger workers

- Modest benefit adjustments for higher-income earners

- Benefit enhancements for low-income recipients, paired with funding changes

None of these is politically easy. But the political math also makes full inaction unlikely — Social Security is one of the most popular programs in America, and cutting benefits by 20% overnight would be electoral poison for any party that allowed it to happen.

That doesn’t mean you should count on Congress. It means that the worst-case scenario — a sudden, unaddressed 23% cut landing with zero warning — is unlikely, even if it’s not impossible.

Should You Claim Social Security Early? Breaking Down the Real Trade-Offs

Okay, this is the heart of the question.

If you claim at 62 instead of waiting until your Full Retirement Age (FRA, which is 67 for most people reading this) or age 70, you’re locking in a permanently reduced benefit. We’re talking about a reduction of up to 30% compared to what you’d get at 67, or up to 43% less than the maximum benefit available at 70.

Let’s put numbers on it again:

| Claim Age | Approximate Benefit (vs. FRA) |

|---|---|

| 62 | ~70–75% of your FRA benefit |

| 67 (FRA) | 100% of your FRA benefit |

| 70 | ~124% of your FRA benefit |

So if your FRA benefit would be $2,000/month, claiming at 62 might give you $1,400–$1,500. Waiting until 70 could give you $2,480.

Now here’s what people get wrong: they think claiming early “locks in” benefits before a potential cut. But it doesn’t protect you — it just permanently reduces your baseline before any potential cut is applied on top.

If benefits are cut 20% in 2033 and you claimed at 62, you’d be taking a 20% hit on an already-reduced amount. You’ve essentially doubled down on a lower number.

When Claiming Early Does Make Sense

To be fair, there are legitimate reasons to claim at 62 that have nothing to do with panic:

- Poor health or shorter life expectancy — if you don’t expect to live past your mid-70s, early claiming often makes mathematical sense

- Financial need right now — if you genuinely need the income and have no other option

- A high-earning spouse delaying their own benefits — in some dual-income strategies, one spouse claims early while the other waits to maximise the higher benefit

These are real, valid reasons. But fear of a funding cut isn’t the same as any of those.

Why Claiming Early “Just in Case” Can Backfire

Think of it this way: claiming at 62 to avoid potential future cuts is like selling your house at a 25% discount because you heard housing prices might drop someday.

You’ve already taken a guaranteed, permanent loss to avoid an uncertain, possibly never-happening one. If Congress fixes the problem (which is more likely than not, based on historical precedent), you’ve permanently reduced your lifetime benefits for nothing.

The break-even point — the age at which delaying actually pays off more than claiming early — sits around 80–82 when comparing age 62 vs. 70 claims. If you live past that — and Americans are living longer than ever — waiting almost always wins financially.

How to Prepare Financially If Social Security Benefits Are Reduced

Whether or not you decide to adjust your claiming strategy, here are the concrete steps worth taking in 2025:

1. Get your personalised Social Security estimate. Log in at SSA.gov and review your earnings record and projected benefit at 62, 67, and 70. Seeing your actual numbers changes the abstract into something real.

2. Build a financial buffer that doesn’t depend on Social Security alone. Even a modest $20,000–$30,000 in accessible savings could cover a year or two of a benefit reduction while Congress figures things out.

3. Run the break-even math for your specific situation. Your health, spouse’s income, other assets, and spending needs all affect the right answer. A fee-only financial planner (not a commission-based one) can run this in an hour.

4. Stop making permanent decisions based on temporary uncertainty. The funding cliff is real. But it’s also years away, and the policy landscape between now and 2033 will shift — probably multiple times.

5. If you’re 62–64 right now and considering early claiming, at minimum, wait until you’ve had a calm, numbers-based conversation with a financial professional before filing. Don’t let anxiety be the deciding factor for a choice you can’t undo.

Some retirees are also supplementing their income through international freelance work, which has become far more accessible in recent years. If that’s a path you’re considering, it’s worth understanding the legal side before you start — particularly around contracts, payment terms, and jurisdiction clauses. This guide to international freelance contracts walks through the key protections you’ll want in place when working with clients across borders.

And if your supplemental income involves selling products or services online — even part-time — the payment infrastructure you use matters more than most people realise. Handling transactions in multiple currencies without the right setup can quietly eat into your margins through conversion fees and processing delays. A multi-currency payment gateway built for small e-commerce can make a real difference if you’re scaling beyond a single market.

FAQs

If Social Security benefits are cut in 2033, will it affect people already collecting?

Technically, yes — under current law, that automatic reduction would hit everyone’s check. But here’s the reality: most policy experts and historical patterns suggest Congress moves before that ever fully lands on current retirees. The 1983 precedent is the clearest example of Washington acting at the last minute to protect beneficiaries already in the system. Possible? Yes. Inevitable? Far from it.

Is claiming at 62 a way to “lock in” benefits before cuts hit?

Not really. Claiming at 62 permanently reduces your base benefit by up to 30%. If a future cut is applied on top of that, you’re taking the hit on an already-smaller number. Claiming early only makes strategic sense if you have health concerns, immediate financial need, or a specific spousal strategy in play.

What’s the most likely Congressional fix for Social Security?

No one knows for certain, but the most frequently discussed options are raising or removing the payroll tax cap and modest adjustments to benefits for higher earners. A combination approach — like the 1983 fix — is historically how these situations get resolved.

At what age does delaying Social Security benefits stop making financial sense?

The break-even point — where delayed claiming pays off more than starting early — is typically around age 80–82 when comparing a claim at 62 vs. 70. If you have significant health issues or a family history of shorter life expectancy, earlier claiming may be mathematically better for you specifically. For most people who are reasonably healthy, longer is generally the more financially rewarding path.

No Comment! Be the first one.