Small business uncertainty just hit a level most owners have never seen. The NFIB Uncertainty Index climbed to 91 in May 2026, well above its long-run average of 68, while the Optimism Index slipped to 95.3, below its 52-year average of 98.0. If you run a business, you already know what that uncertainty feels like — a late client payment, a broken espresso machine, a software renewal that lands at the worst possible time.

The numbers behind that feeling are stark. Twenty-two percent of Americans have no emergency savings at all, and 37% of adults say they struggle to cover a surprise $400 expense. For an entrepreneur, that gap isn’t just a personal problem; it puts payroll, vendor payments, and the business itself at risk.

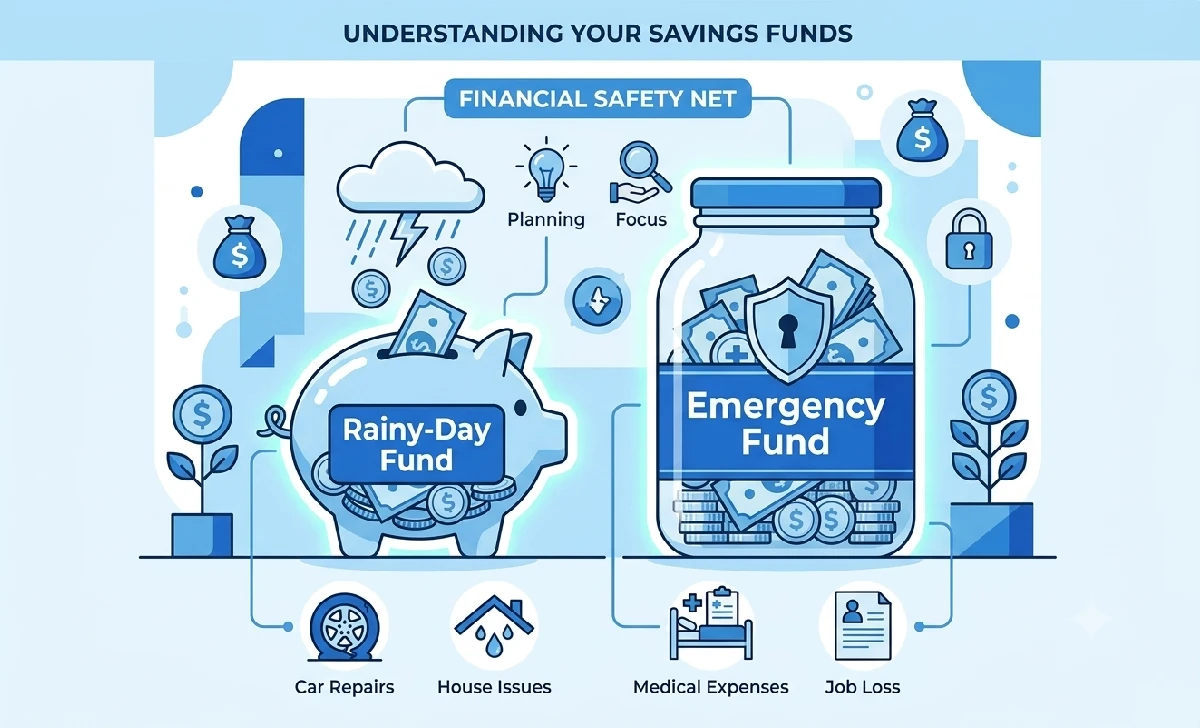

A rainy-day fund is your first line of defence. This guide walks through what it is, how it differs from a true emergency fund, how much to save, and seven practical ways to build one — even if your margins are thin.

Key Takeaways

- A rainy-day fund covers midsize, unexpected expenses — it’s smaller and more frequently used than a full emergency fund.

- Start with one month of operating expenses as your first goal, then build toward three to six months.

- Automate your contributions so saving happens without relying on willpower.

- Keep the fund in a separate, liquid, high-yield account, not your operating account.

- With uncertainty at historic highs, this fund is a core business discipline, not a someday project.

What Is a Business Rainy-Day Fund?

A business rainy-day fund is cash set aside to cover midsize, non-routine expenses and short-term disruptions — the kind of costs that aren’t part of your regular budget but aren’t catastrophic either. Think of it as a buffer between “normal month” and “true emergency.”

Common examples include a broken piece of equipment, a 30–60-day delay on a client invoice, a surprise licensing renewal, or a short seasonal 60-day revenue. What it isn’t: a fund for planned purchases, growth investments, or routine operating costs like rent and payroll. Those belong in your regular budget, not your reserve.

Rainy-Day Fund vs. Emergency Fund: Why You Need Both

These two terms get used interchangeably, but they serve different purposes. A rainy-day fund is smaller — typically $500 to $5,000 — and gets tapped a few times a year for minor surprises. A business emergency fund is larger, usually three to six months of operating expenses (some advisors now recommend six to twelve months given current conditions), and is reserved for major disruptions like losing a key client or facing a natural disaster.

There’s also a personal layer to consider. A personal emergency fund covers your household if your income drops; a business emergency fund covers payroll, rent, and supplies if the business itself hits a wall. In a severe downturn, you may need both at once.

| Feature | Rainy-Day Fund | Business Emergency Fund | Personal Emergency Fund |

| Purpose | Midsize, unexpected business costs | Major business disruptions | Personal financial emergencies |

| Size | $500–$5,000+ | 3–6 months of operating costs | 3–6 months of living costs |

| Used | A few times a year | Rarely, true emergencies only | Rarely |

| Example | Equipment repair, short revenue dip | Loss of a major client, disaster | Job loss, medical bill |

Why Entrepreneurs Need This Fund Right Now

The NFIB data isn’t abstract. Optimism is below its historical average and uncertainty is well above it, and rising costs for labor, insurance, and operations are squeezing margins across nearly every industry. Without reserves, business owners often turn to credit cards or short-term loans to cover gaps — a move that compounds the original problem with interest.

Picture a business owner whose client pays 60 days late. Without savings, $15,000 lands on a credit card at 22% APR, adding roughly $550 in interest over six months for a problem that reserves would have absorbed for free. A rainy-day fund lets you pay employees, maintain operations, and avoid desperate decisions when things get tight.

How Much Should You Save?

Start with one month of operating expenses as your first milestone, then build toward three months and eventually six. Businesses in volatile industries, or those navigating today’s uncertain climate, may want to push toward six to twelve months over time.

To calculate your number: add your fixed costs (rent, payroll, insurance, loan payments) and variable costs (inventory, marketing, utilities) to get your total monthly operating expenses. Multiply that figure by your target number of months. A professional services firm spending $60,000 a month, for instance, would need $180,000 to reach a three-month cushion.

A Simple Worksheet

- List your fixed monthly expenses (rent, payroll, insurance, loans).

- List your variable monthly expenses (inventory, marketing, utilities).

- Add them together for your total monthly operating cost.

- Multiply by your target: 1 month (starter), 3 months (comfortable), or 6+ months (strong).

- Divide that total by the number of months you want to take to reach it — that’s your monthly savings target.

Seven Ways to Build Your Rainy-Day Fund

Saving doesn’t have to mean cutting growth or stretching cash flow to the breaking point. These approaches work even on thin margins.

1. Identify your biggest financial risks

Every business has a different risk profile — late payments, client attrition, equipment failure, seasonal swings, or a cybersecurity incident. List your top five risks; this shapes both your target amount and how urgently you should be saving.

2. Set a realistic starting goal

Don’t wait for a windfall. Even $500 to $1,000 provides a meaningful cushion, and your first real milestone should be one month of operating expenses. Incremental progress beats a perfect plan that never starts.

3. Automate your contributions

Set up a recurring transfer from your operating account to a dedicated savings account, either as a fixed amount each month or a percentage of every deposit. Automating removes the decision — and the temptation to skip it — from the equation.

4. Save a percentage of monthly revenue

Transferring a fixed share of revenue, say 3–10%, naturally scales with your business: lean months contribute less, strong months contribute more, without any manual recalculating.

5. Capitalise on strong periods

When a big contract closes or a past-due invoice finally gets paid, resist reinvesting all of it back into the,business. If a project brings in an unexpected $25,000, setting aside even 20% ($5,000) meaningfully accelerates your fund.

6. Cut or reallocate existing expenses

Audit subscriptions, software licenses, and recurring costs for waste. Redirect anything you cancel or renegotiate straight into the fund — small, consistent reallocations add up faster than they seem.

7. Use windfalls and refunds strategically

Tax refunds, insurance payouts, and legal settlements are ideal fund boosters. Decide in advance to put a set percentage — say 50% — toward your reserve so you’re not negotiating with yourself in the moment.

Where to Keep the Fund

Your reserve should be liquid, insured, and separate from your day-to-day operating account. A high-yield business savings account is usually the best primary option, offering above-average interest while staying accessible. Money market accounts are a solid alternative, sometimes with check-writing privileges. A traditional business savings account is the most accessible option but typically earns the least.

Keeping the fund at a different institution than your operating account adds a useful layer of friction, reducing the chance you’ll dip into it for non-emergencies. Credit unions often offer better rates and lower fees than traditional banks, so it’s worth comparing both.

When (and When Not) to Use It

Set written rules in advance for what qualifies as a legitimate withdrawal: equipment failure, a short-term revenue gap, emergency repairs, or a security incident. Planned marketing campaigns, new hires, or growth inventory don’t belong here — those are budget items, not emergencies. If you have business partners, consider requiring two-person approval for any withdrawal.

After a withdrawal, treat replenishment with the same urgency you gave to building the fund initially. Resume automatic contributions right away, and consider temporarily increasing your savings rate until the balance is restored.

Scaling the Fund as You Grow

Review your fund against current operating expenses at least quarterly — as your costs grow, your target should grow with them. A new business might aim for one month of coverage, a growing company for three, and an established business for six or more. Many businesses eventually run a two-tier system: a smaller rainy-day fund for everyday surprises and a larger emergency fund for major disruptions. Recalibrate annually, or any time something significant changes, like a new office or a new product line.

Build the Habit, Not Just the Fund

With small business uncertainty at historic highs, a rainy-day fund isn’t optional — it’s a basic discipline that protects your team, your operations, and your decision-making. The fund itself matters, but the habit behind it matters more: every automated transfer builds a culture of financial resilience into how your business runs.

This week, calculate your monthly operating expenses. This month, open a dedicated high-yield savings account. This quarter, set up your first automatic transfer. Financial resilience gives you the freedom to make decisions from strength rather than scrambling — and the best time to start building that freedom is now.

FAQs

How much should a small business have in a rainy-day fund?

Start with one month of operating expenses and build toward three to six. Businesses in volatile industries or uncertain conditions may aim for six to twelve months.

Is a rainy-day fund the same as an emergency fund?

No. A rainy-day fund covers smaller, non-routine costs, typically $500 to $5,000. An emergency fund is larger and reserved for major disruptions like losing a key client or facing a disaster. Ideally, you have both.

Where should I keep my business rainy-day fund?

A high-yield business savings account or money market account is usually best — liquid, insured, and earning interest, while staying separate from your operating funds.

How do I build a fund with very thin margins?

Start small, even $50 to $100 a month. Automate the transfer so it happens before you can spend the money, and route savings from cancelled subscriptions or strong revenue periods straight into the fund. Consistency matters more than size.

Should I invest my rainy-day fund in the stock market?

No. The fund needs to stay liquid and accessible. Investments carry volatility risk and may not be available exactly when you need them, so keep this money in insured, liquid accounts.

This article is for general informational purposes and isn’t financial advice. Consult a financial advisor or accountant for guidance specific to your business.

No Comment! Be the first one.