You claimed the Employee Retention Credit a while back. Now a letter from the IRS mentions something called OBBA, and it says your claim is denied. This guide explains what OBBA actually is, who it affects, and what you can do next.

OBBA stands for the One Big Beautiful Bill Act. Congress passed it, and the president signed it into law on July 4, 2025. Its official citation is Public Law 119-21. It is a large federal tax and spending law, and one small part of it, Section 70605(d), deals directly with the Employee Retention Credit.

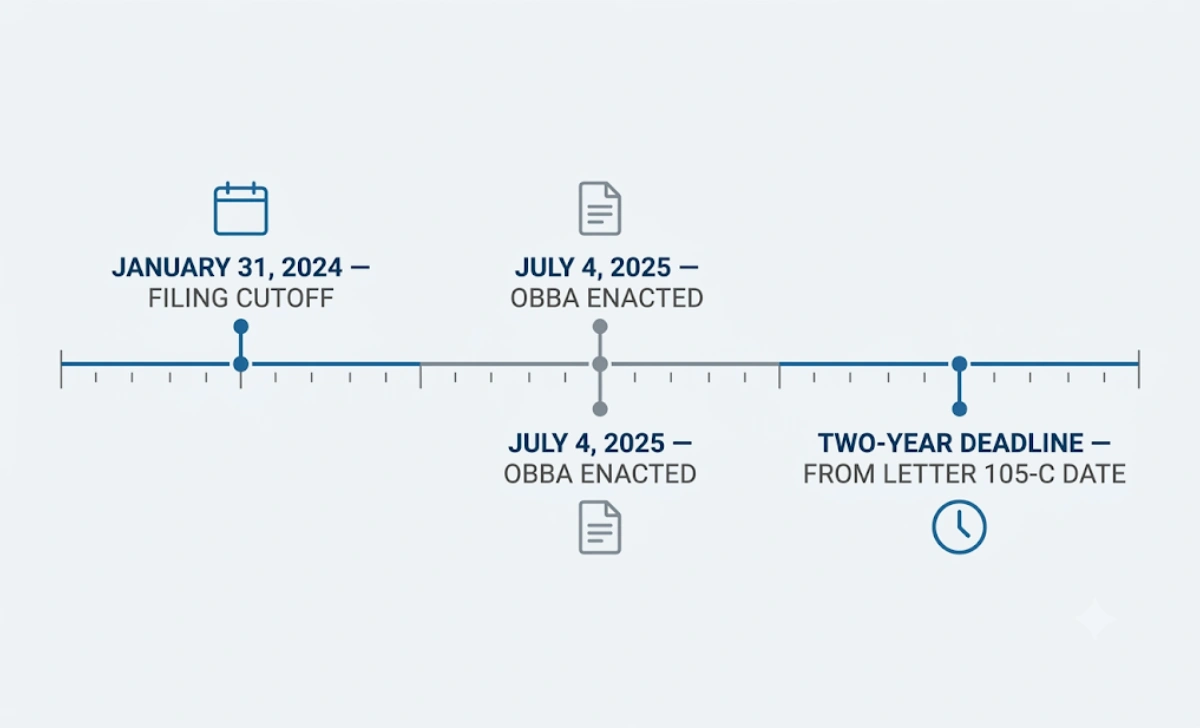

Before this law, eligible businesses could file Form 941-X to claim the ERC for wages paid between March 13, 2020, and December 31, 2021. The deadline to claim the credit for 2021 quarters was April 15, 2025. Many businesses filed close to that date, and some filed even later, believing they still had time or unaware the deadline had passed.

Section 70605(d) targets a narrow group: claims for the third and fourth quarters of 2021 that were filed after January 31, 2024. If the IRS had not already paid or approved one of those claims by July 4, 2025, the law now prevents the IRS from allowing or refunding it, even if the business met every eligibility rule.

The law also extended how long the IRS can examine a Q3 2021 ERC claim. Before OBBA, the IRS had five years from the later of your return’s filing date or its deemed filing date. Now it has six years, measured from the latest of three dates: when you filed the original return, the deemed filing date, or the date you filed the Form 941-X claiming the credit.

Who Is Affected by the OBBA ERC Limitation

This rule applies narrowly. It only touches ERC claims for the third and fourth quarters of 2021. Claims for 2020 quarters, or for the first two quarters of 2021, are not affected by Section 70605(d).

Within that window, two groups feel the impact:

- Businesses that filed a Q3 or Q4 2021 ERC claim after January 31, 2024, and the IRS had not paid or approved it before July 4, 2025.

- Businesses that activated a previously filed protective claim after January 31, 2024. A protective claim is one filed to preserve your rights while the exact eligibility details are still being worked out.

If you filed your claim on or before January 31, 2024, this limitation should not apply to you, even if you later receive a letter that mentions OBBA. That situation is common enough that the IRS has a specific process for it, covered below.

Dealing with a stalled ERC claim is also a good moment to look at how well your business tracks documents and deadlines in general. If your recordkeeping felt disorganised during this process, it may be worth reviewing your operational infrastructure as your business scales, since the same systems that keep a growing company organised will help you respond to IRS deadlines faster next time.

One more group to know about: if you filed an amended return after January 31, 2024, specifically to withdraw an ERC claim you no longer believe you qualify for, Section 70605(d) does not stop the IRS from processing that withdrawal.

What Happens When Your Claim Is Disallowed

If the IRS disallows your ERC claim, whether because of OBBA or for another reason, you will receive Letter 105-C, Claim Disallowed (or Letter 106-C if only part of the claim is denied). This letter tells you:

- The reason the IRS denied your claim.

- The date of the decision.

- Which tax period the denial covers.

- Your appeal rights.

- The deadline to file suit if you want to challenge the decision in court.

You generally have two years from the date on Letter 105-C to resolve the issue with the IRS or to file a refund suit in federal court. Filing an administrative appeal with the IRS Independent Office of Appeals does not pause this two-year clock. If the two years run out before you file suit or reach a written agreement to extend it, the IRS cannot issue a refund, even if it later agrees you were right.

If your claim was disallowed specifically under Section 70605(d) and you believe your claim was actually filed on or before January 31, 2024, you can appeal to the Independent Office of Appeals. Bring proof of timely filing, such as a certified mail receipt, an e-file confirmation, or another record showing when you submitted the claim.

A New Way to Buy More Time: Form 907

Many taxpayers who protested a disallowance are still waiting on the IRS while their two-year deadline quietly ticks away. To address this, the IRS now allows certain taxpayers to request an extension using Form 907, Agreement to Extend the Time to Bring Suit.

You may qualify for this option if both of the following are true:

- You already responded to your Letter 105-C or 106-C and are still waiting for the IRS to review that response.

- You have six months or less remaining before your two-year deadline expires.

Some eligible taxpayers automatically receive IRS Notice CP320B inviting them to use this process. But you do not need to wait for that notice. You can submit Form 907 through the IRS Document Upload Tool by selecting notice “CP320B” from the dropdown menu, even if you never received one. The extension is not valid until the IRS reviews it and sends back a signed copy, so submit it well before your deadline and keep a record of what you sent.

If you already have an assigned Appeals Officer working your case, contact that person directly to discuss an extension instead of using the upload tool.

Special Situations

You filed before January 31, 2024, but still got an OBBA denial

Some businesses that filed on time are receiving disallowance letters that mention OBBA anyway, likely due to how claims were logged. If this happens to you, respond to the letter with clear proof of your original filing date and formally dispute the denial.

You activated a protective claim

If you filed a protective claim before the deadline but did not activate, or formally pursue, it until after January 31, 2024, the IRS may treat the activation date as your filing date for OBBA purposes. If you believe your protective claim itself was timely filed, make that argument in writing when you respond.

You want to withdraw your claim

The ERC withdrawal program is still available for claims that have not been paid or processed yet. If you now have doubts about your eligibility, withdrawing may be simpler than waiting for a disallowance and going through the appeal process. Note that if you already received Letter 105-C, you are not eligible to withdraw for that specific tax period, though you may still be able to withdraw claims for other quarters.

If your business was counting on this credit and now faces a gap, it helps to have a cushion for situations like this. Our guide on how entrepreneurs build a rainy-day fund that actually protects their business walks through practical ways to set money aside so an unexpected denial does not put your operations at risk.

Steps to Take Now

- Check the filing date on your original ERC claim against January 31, 2024, and gather proof of when you filed.

- If you receive Letter 105-C or 106-C, read it carefully and note the exact date, since that starts your two-year clock.

- Decide whether to appeal, and if you do, include documentation supporting your eligibility and, if relevant, your timely filing.

- If you are close to your two-year deadline and still waiting on the IRS, look into Form 907 well ahead of time.

- Talk with a CPA or tax attorney who has handled ERC cases, especially if the dollar amount is significant.

- Keep every document related to your claim: your Form 941-X, wage calculations, government orders you relied on, and all IRS correspondence.

Where This Stands Now

The IRS has been working through a large backlog of ERC claims, and OBBA-related denials are part of that process. If you get a letter mentioning OBBA and you are not sure whether it applies to your situation, do not ignore it. Check the filing date, read your appeal rights carefully, and respond within your deadline. Waiting can cost you the credit entirely, regardless of how strong your original claim was.

Tax rules are not the only thing changing quickly for business owners right now. If you want to understand another fast-moving shift, our complete 2026 guide to artificial general intelligence looks at how AI capabilities are already affecting knowledge work and what that could mean for how you run your business.

FAQs

What does OBBA stand for?

OBBA stands for the One Big Beautiful Bill Act, a federal law signed on July 4, 2025. It is sometimes written as OBBBA.

Does OBBA affect all ERC claims?

No. Section 70605(d) of OBBA only limits claims for the third and fourth quarters of 2021 that were filed after January 31, 2024 and had not been paid or approved by July 4, 2025.

What if I already got my ERC refund?

If your claim was paid or credited before July 4, 2025, Section 70605(d) does not apply to it, even if you filed after January 31, 2024.

How long do I have to respond to an ERC disallowance?

Generally, two years from the date on Letter 105-C or 106-C. Filing an appeal does not pause this deadline, though Form 907 may extend it in some cases.

Can I still withdraw my ERC claim?

The withdrawal program remains open for claims that have not yet been paid or processed. Once you receive Letter 105-C for a period, that period is no longer eligible for withdrawal.

Do I need a lawyer to fight an OBBA-related denial?

Not always, but it helps for larger claims or if you plan to file suit. A tax professional can also help you gather the right proof of your original filing date.

This article is for general information only and is not tax or legal advice. ERC and OBBA rules can change, and your situation may involve details not covered here. Talk with a qualified CPA or tax attorney about your specific claim.

No Comment! Be the first one.